Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

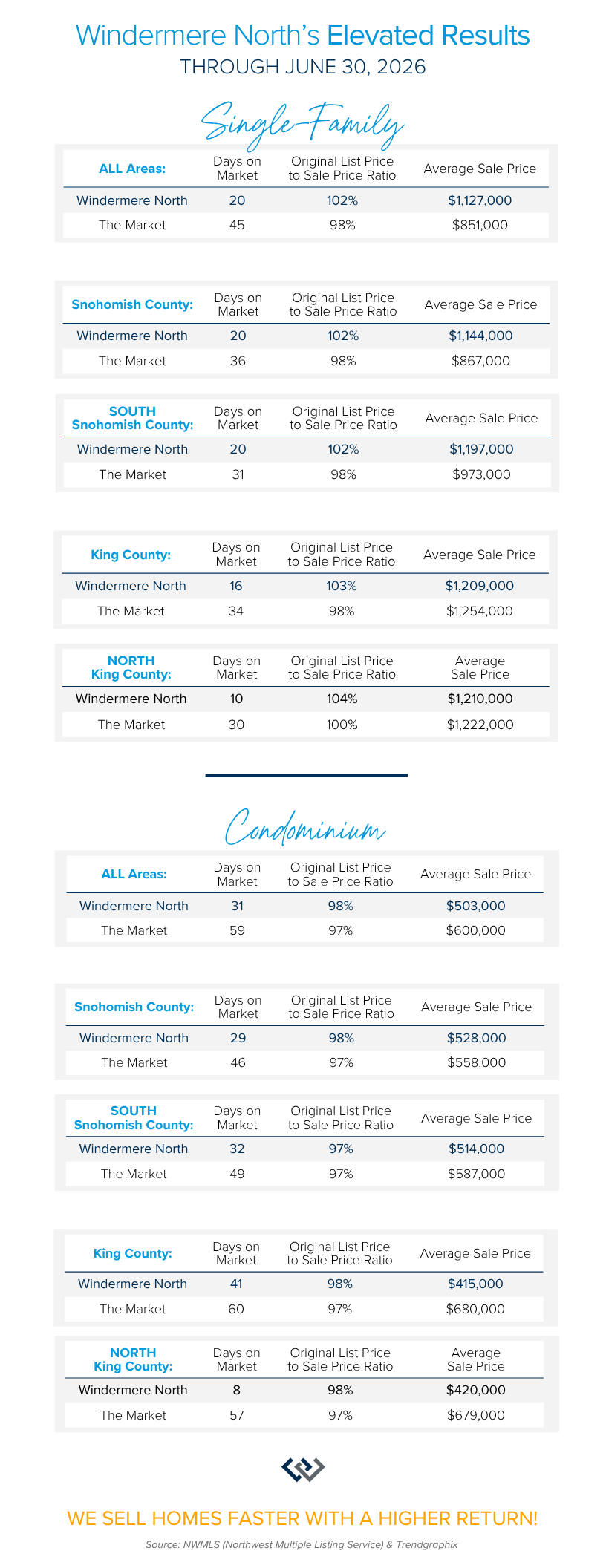

Exceptional Results Start with Exceptional Representation

Every real estate market is different. Some move at lightning speed, while others require patience, strategy, and precision. Today’s market demands more than simply putting a home on the MLS or writing an offer, it requires being rooted in the data and understanding buyer behavior, pricing strategically, knowing when to negotiate, and positioning a home to stand out.

That’s why the experience and resources behind your representation matter.

Through June 2026, homes represented by my office, Windermere North, sold considerably faster than the broader market while also achieving stronger sale-price-to-original list-price ratios. Across the areas we serve, listings averaged 16–20 days on market, compared with 30–45 days for the market overall, while achieving 102–104% of original list price versus 98–100% across the broader market.

I’m fortunate to be part of an office that consistently invests in market knowledge, marketing, technology, collaboration, and professional development. Just as important, I believe those resources only make a difference when paired with personal attention, thoughtful strategy, and a genuine commitment to each client’s goals.

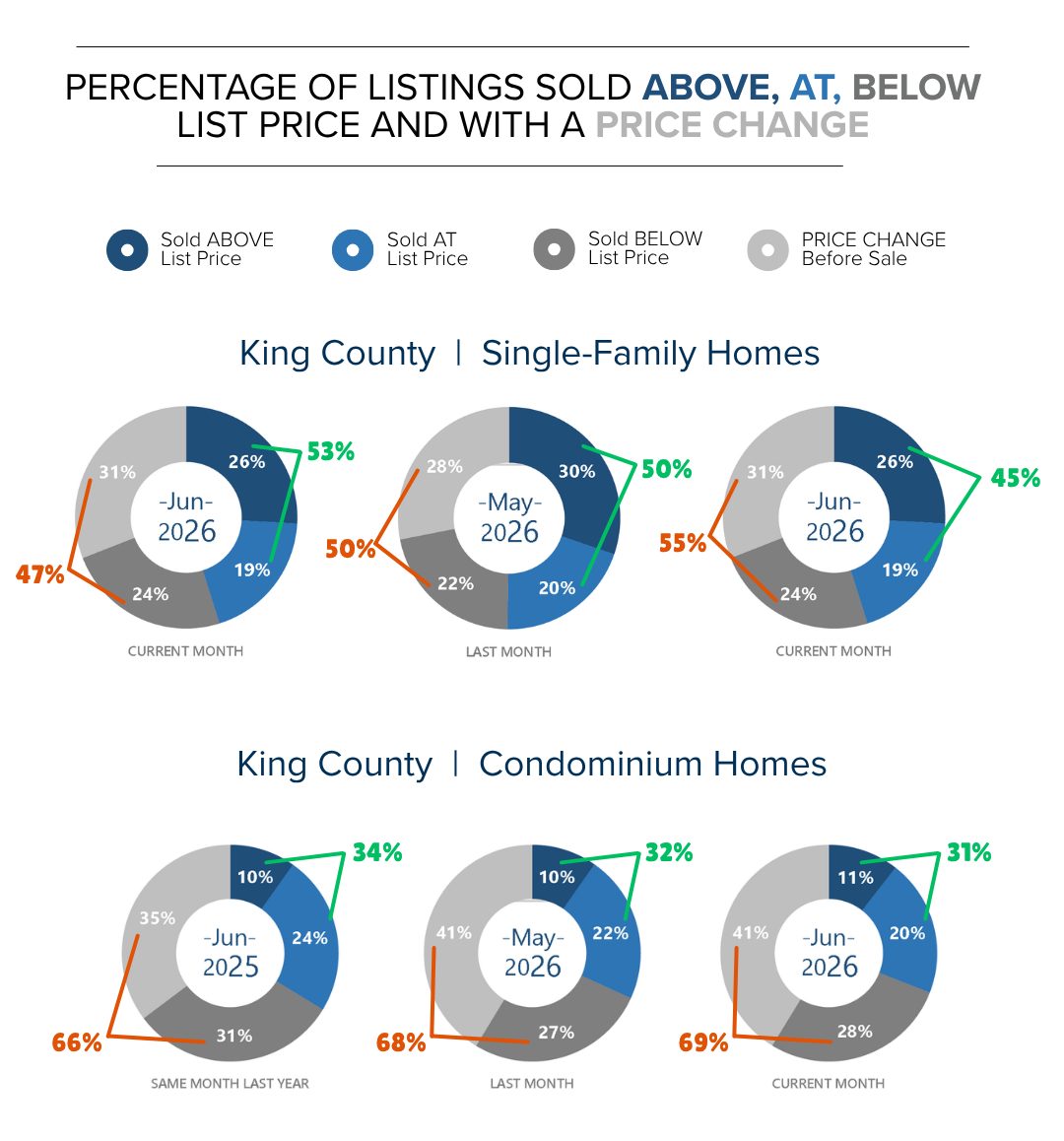

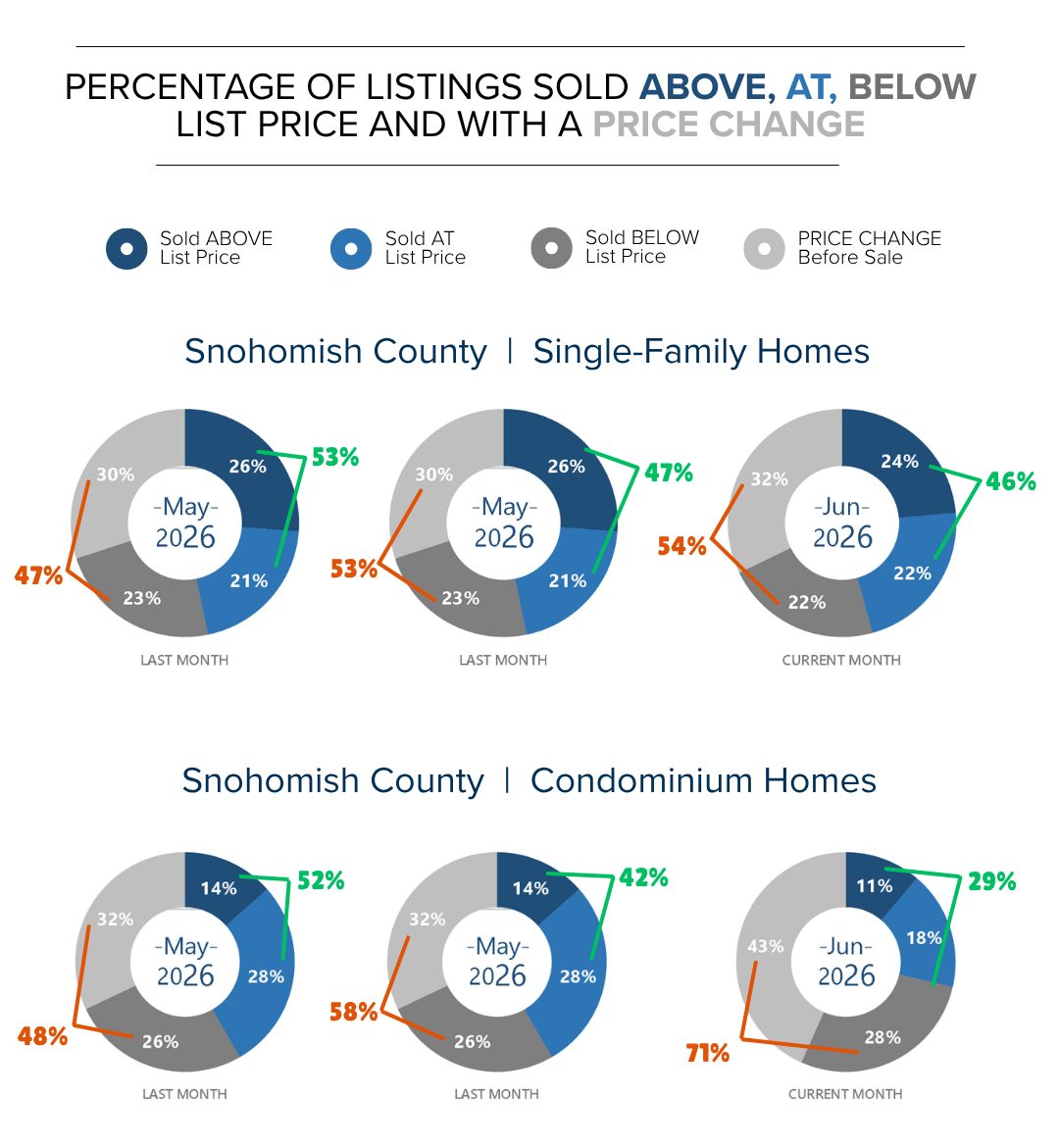

Those numbers aren’t about one individual, they’re the outcome of a thoughtful process and are measurable to our clients’ positive bottom line. As you can see from the chart below, nearly half of the single-family residential sales in King and Snohomish counties are selling at or above list price and the other half are selling under list price or taking price reductions. For condos, a third are selling at or above list price, and the other two thirds are selling for under or taking price reductions.

The opportunity to find yourself in the blue versus the grey comes from careful preparation, accurate pricing, exceptional presentation, strategic marketing, skilled negotiation, and clear communication from beginning to end. It also comes from having someone who understands how markets change and knows when to adapt the strategy. This all starts in asking lots of questions, hearing your goals, and devising a plan that will work in today’s market. With higher inventory (buyers: you have some awesome opportunities right now), it is critical that no steps are skipped in regard to property preparation and that pricing is dialed.

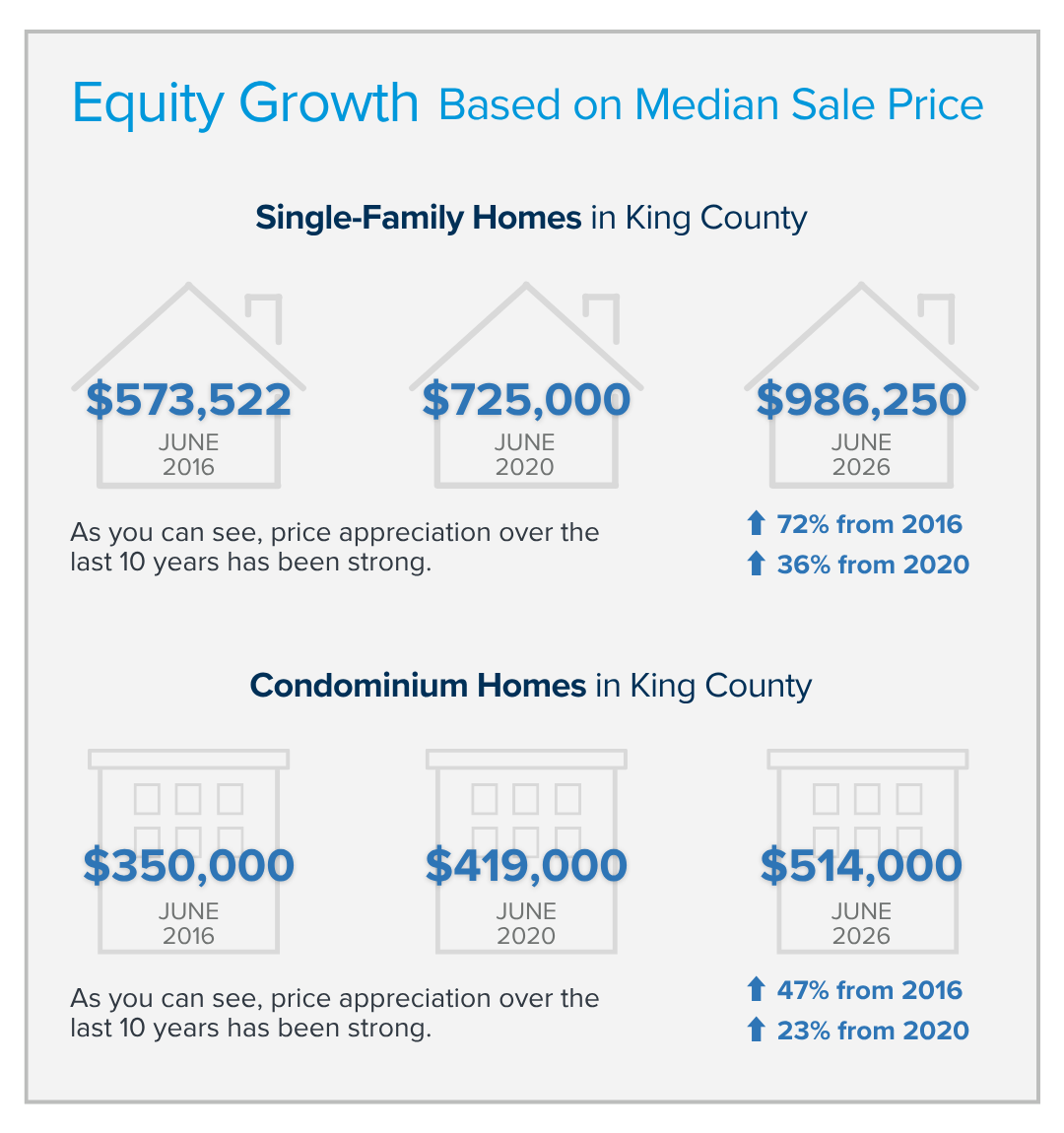

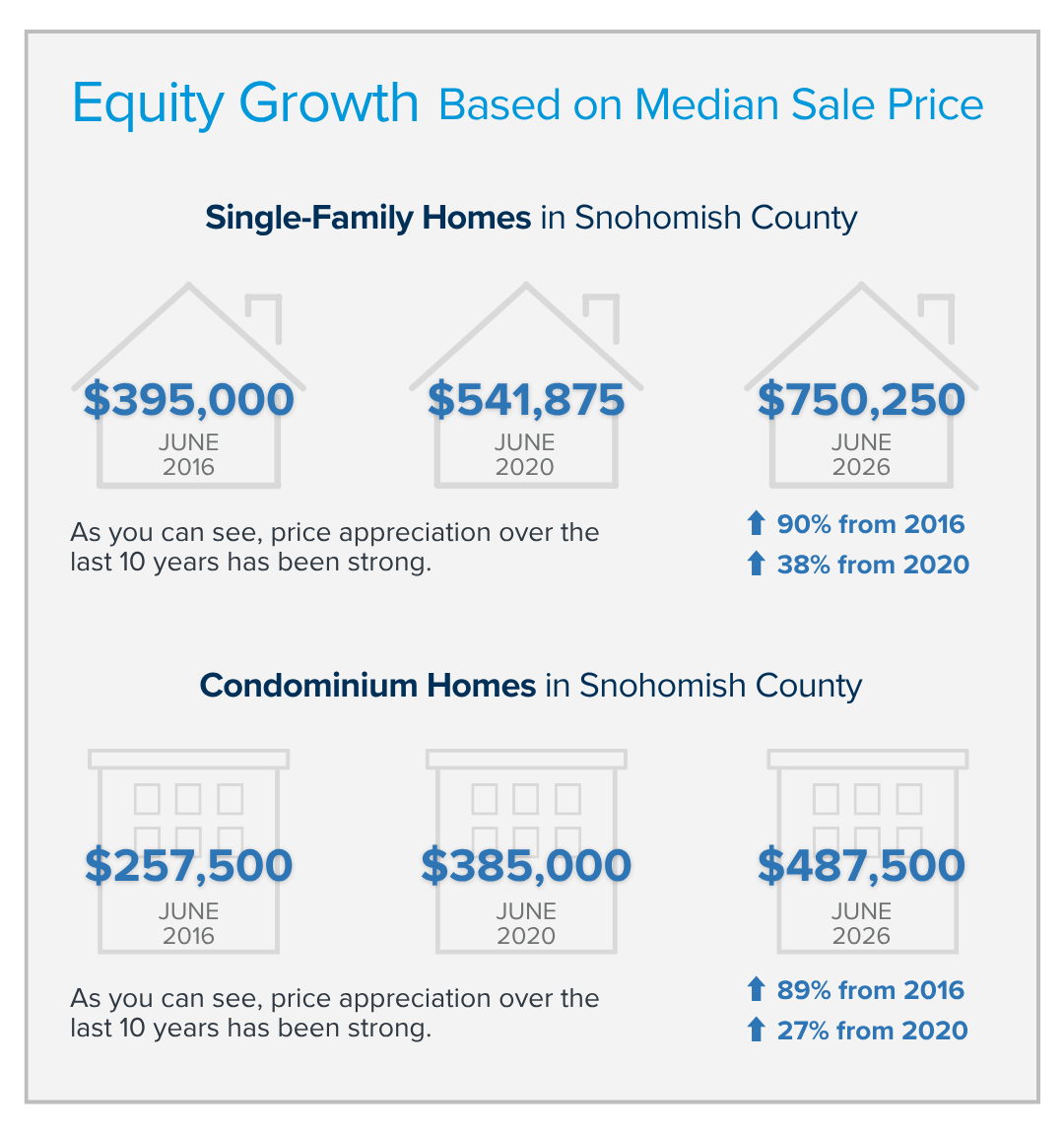

Another important aspect to consider is the long-term equity growth we have seen in our area. While prices have been flat year-over-year and in some cases down slightly, the growth displayed in the graphs below show the immense equity growth over the last 5-10 years. Further, if you have been in your home longer than 10 years, the options to reposition this wealth into a home that better fits your current lifestyle are plentiful.

Whether you’re buying your first home, selling a place you’ve loved for years, or making your next investment, you deserve someone who is continually studying the market, paying attention to the details, and advocating for your best interests every step of the way.

Real estate is one of the most significant financial decisions most people make. The right guidance can make a meaningful difference, not only in the final outcome, but in how confident and supported you feel throughout the process.

For me, that’s what experience is really about. It’s not about years in the business or accolades. It’s about showing up prepared, working diligently, staying informed, and caring deeply about helping clients make smart decisions, no matter what kind of market we’re in.

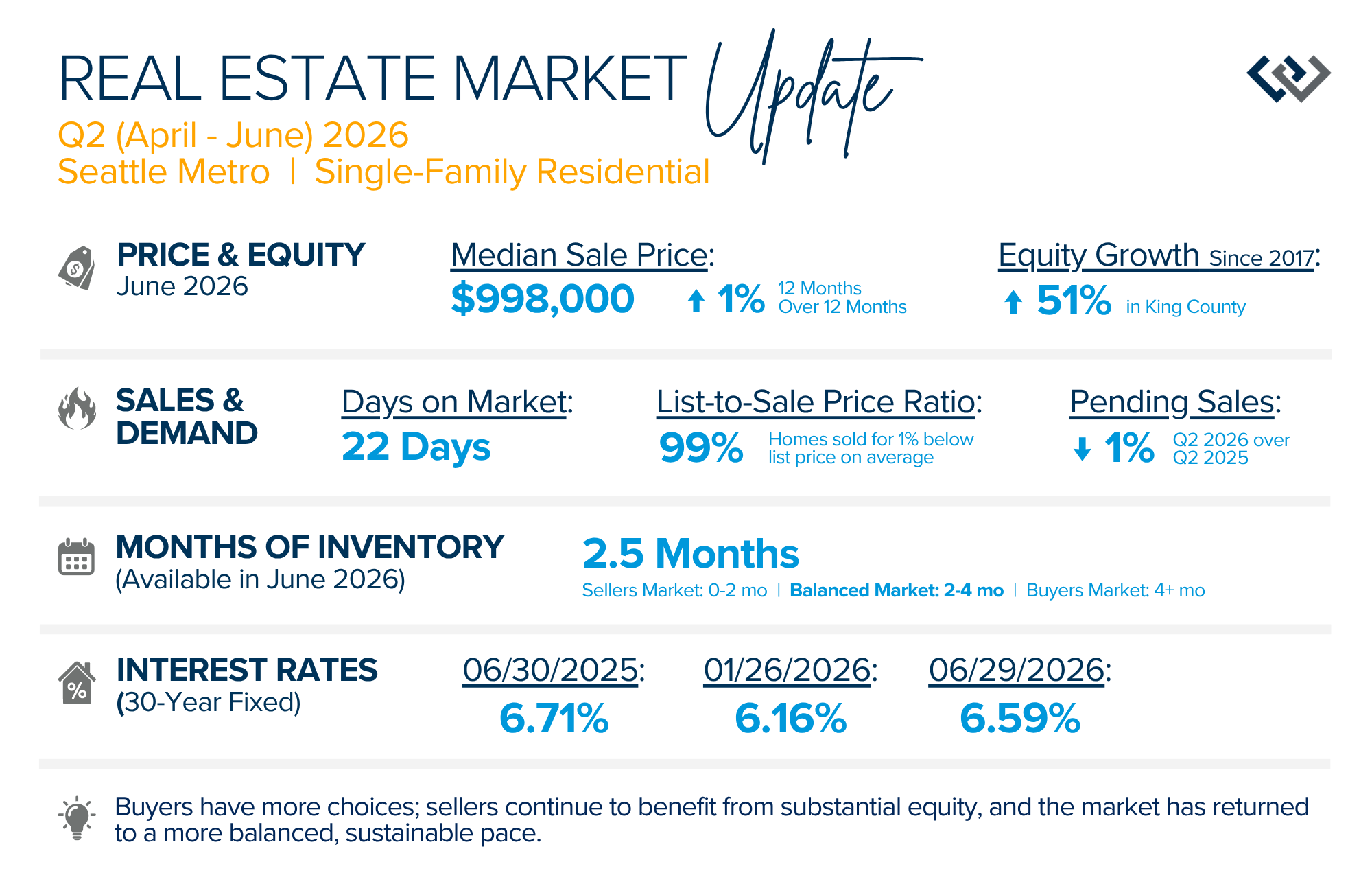

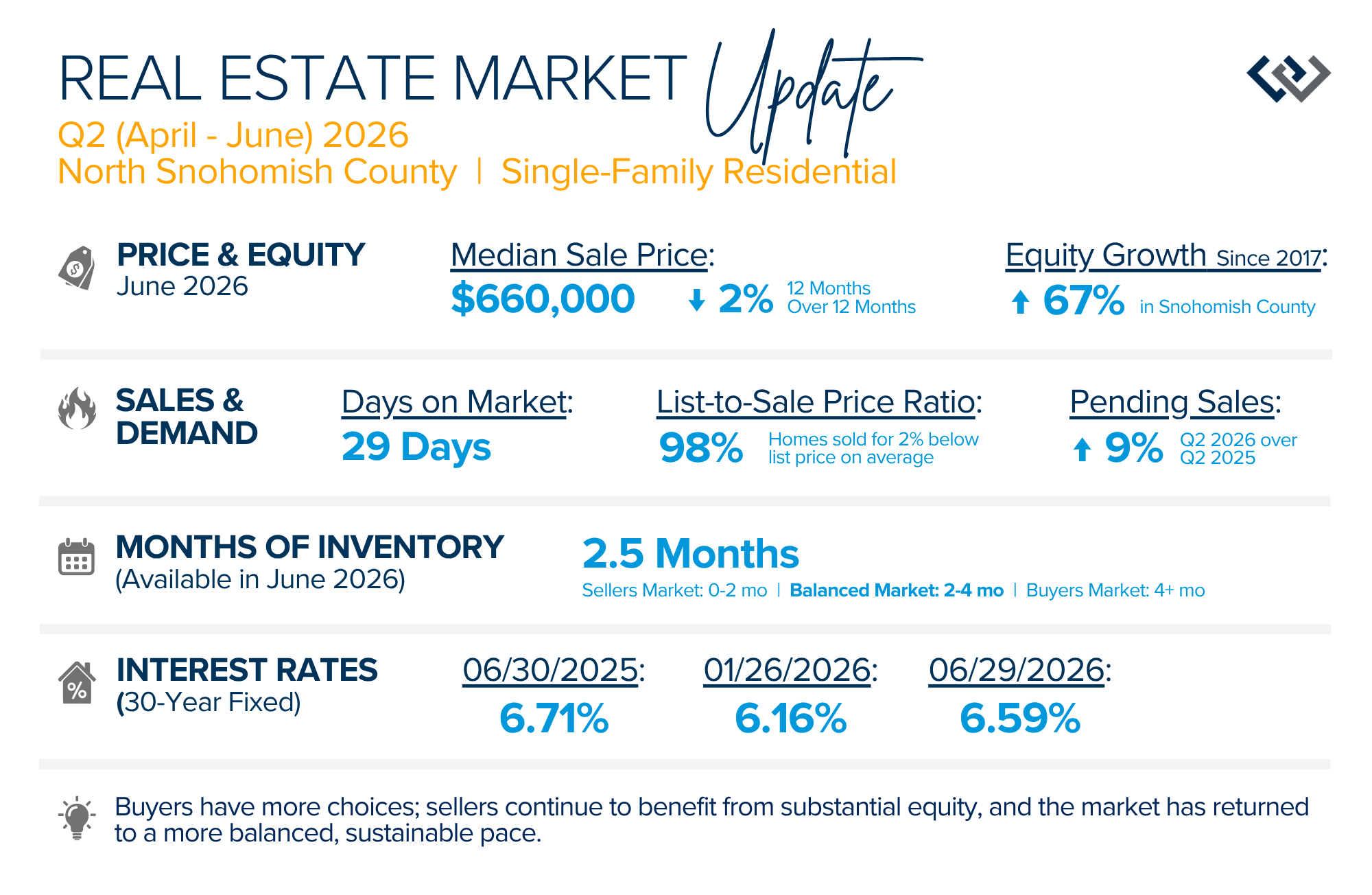

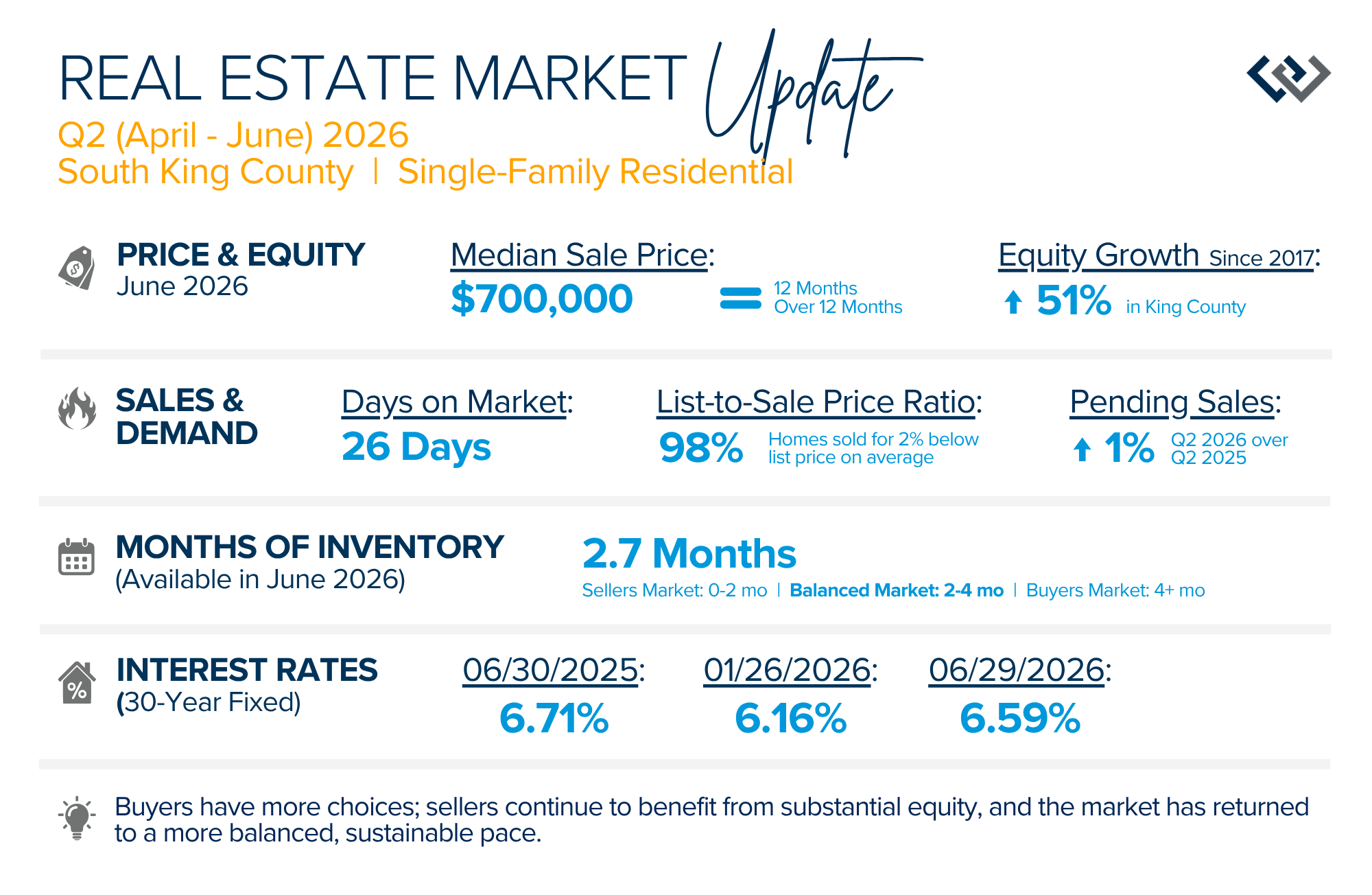

QUARTERLY REPORTS Q2 2026

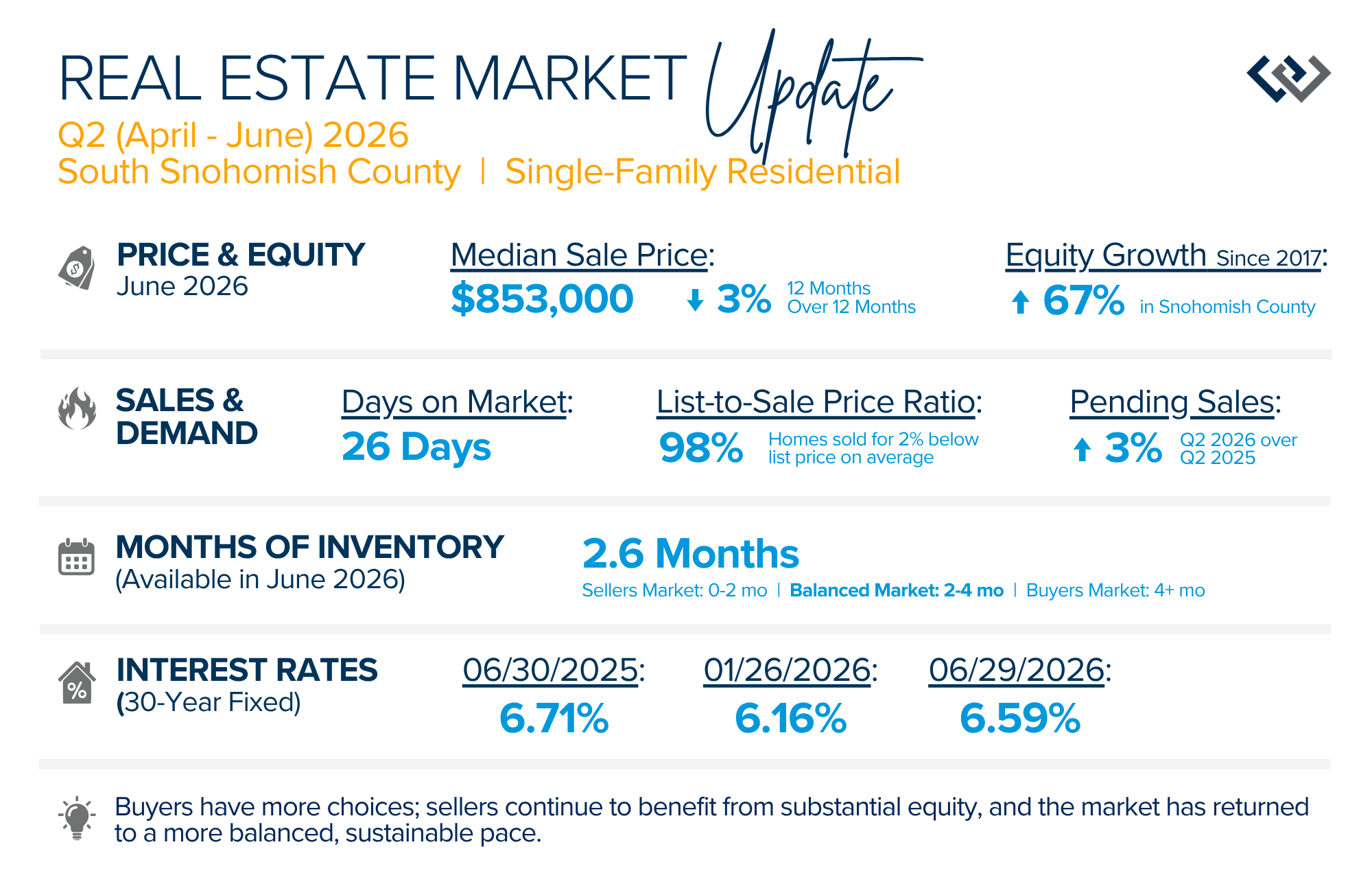

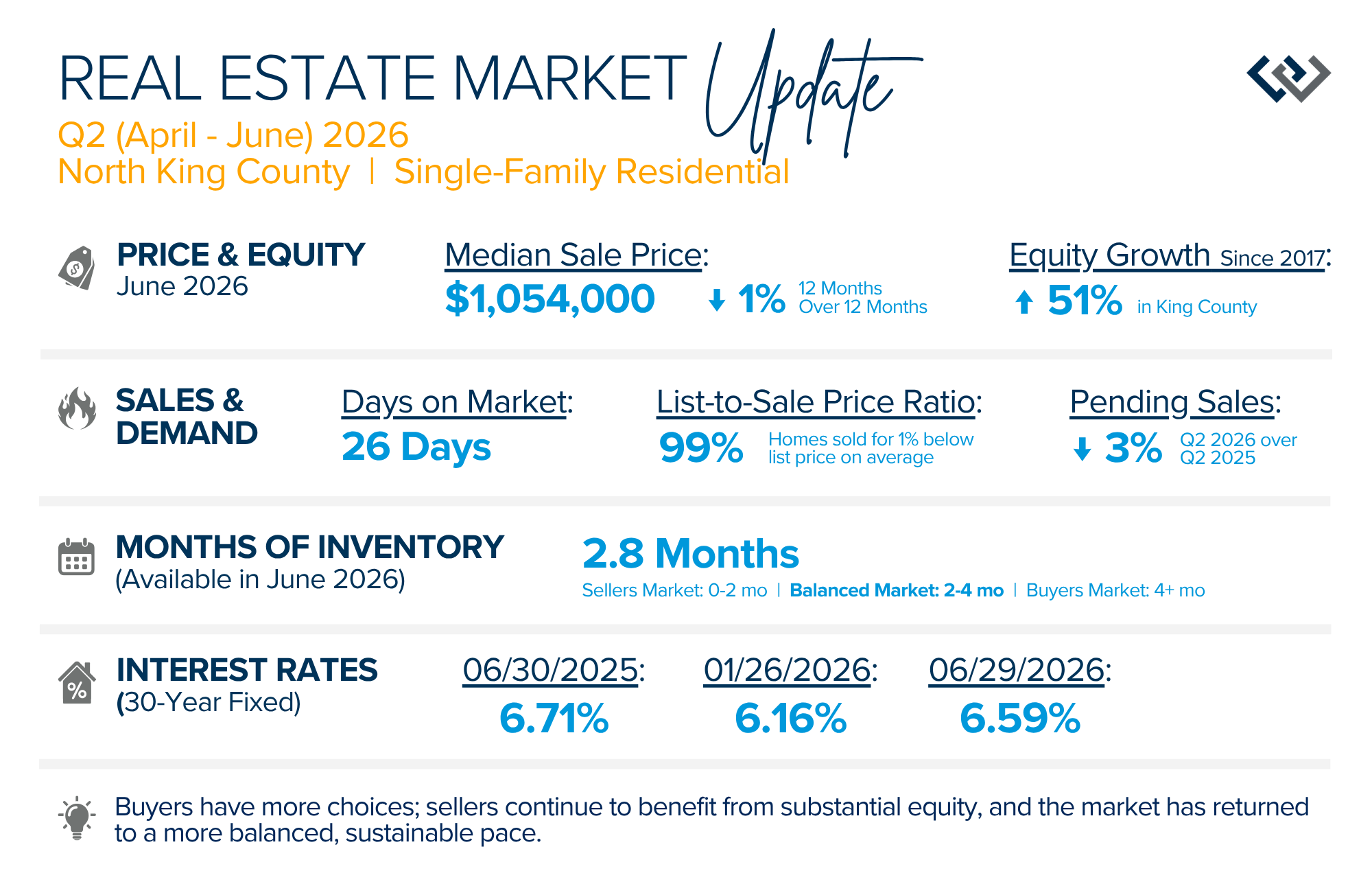

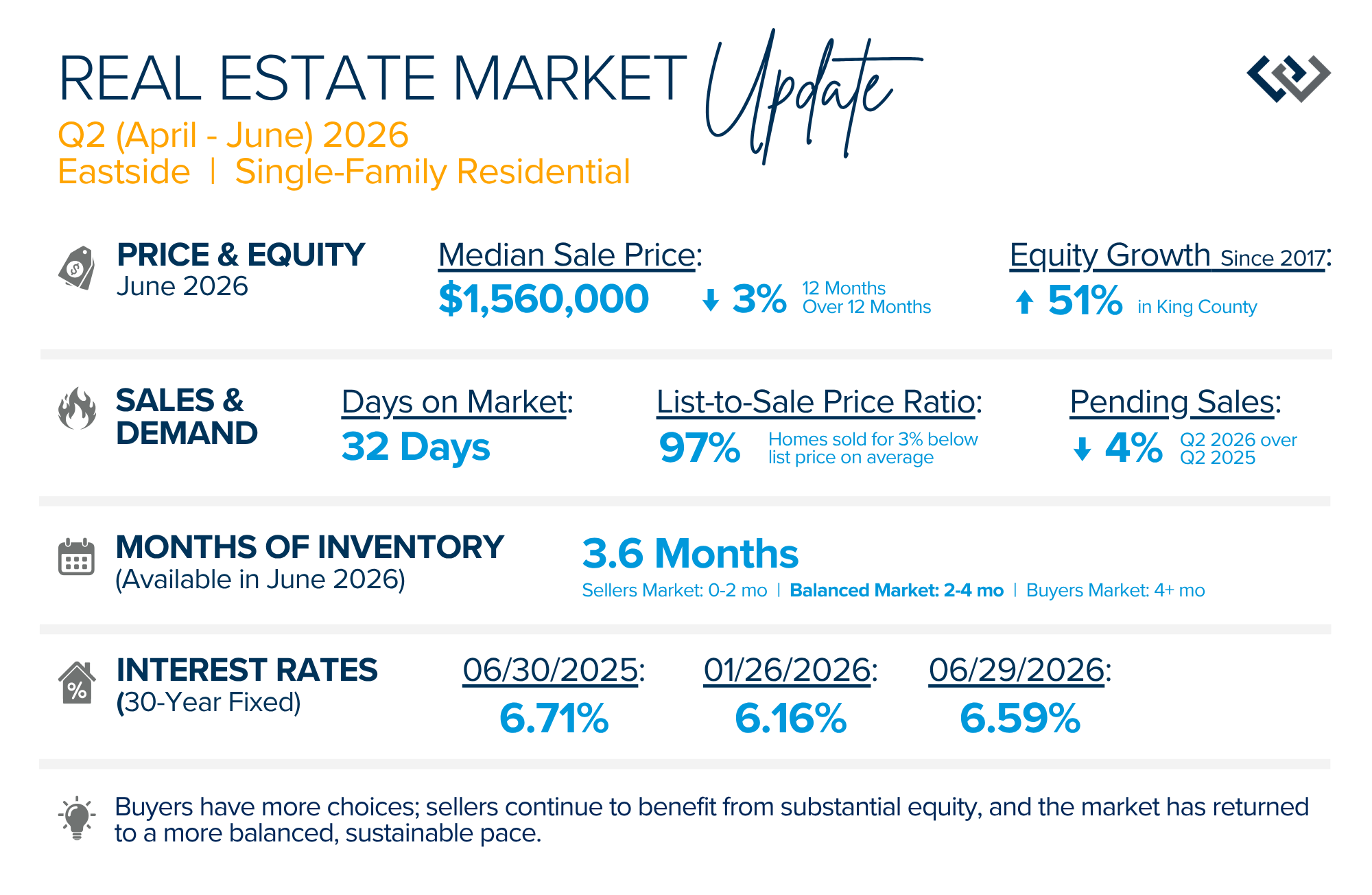

While home values have leveled off after years of remarkable appreciation, today’s market is healthier than many realize. Buyers have more choices; sellers continue to benefit from substantial equity, and the market has returned to a more balanced, sustainable pace. In fact, since 2017, the median home price has grown by 67% in Snohomish County and 51% in King County.

Real estate has always been a long-term investment, and today’s market continues to reward strategy over speed, not perfect timing. Whether you’re buying, selling, or simply planning ahead, understanding the data to gain perspective is key. Whether you’re curious about your home’s current value or considering a move in the future, I’m here to help keep you informed to empower strong decisions.

Seabrook, WA: Your Next Great Escape

Summer has arrived, and if you are looking for a great escape only 3 hours from Seattle, you should check out Seabrook on the Washington Coast! I had the opportunity to enjoy it this winter, and I am excited to share all the aspects this gem of a town has to offer, along with a discount you can use for your stay. This town can be enjoyed through all four seasons, but summer has to be amazing!

I can extend to you a 20% discount off your stay. Seabrook and Windermere  have partnered, and Windermere has become the official real estate company representing Seabrook. This partnership allows us to pass on this discount to our clients who would like to visit. If you are interested in receiving the discount, please reach out, and I can get you registered and personally connect you with the Seabrook rental team to ensure you get to enjoy this special offer.

have partnered, and Windermere has become the official real estate company representing Seabrook. This partnership allows us to pass on this discount to our clients who would like to visit. If you are interested in receiving the discount, please reach out, and I can get you registered and personally connect you with the Seabrook rental team to ensure you get to enjoy this special offer.

Seabrook is a beach town along the Washington Coast’s Olympic Peninsula that is seamlessly woven into nature. The town sits on a scenic bluff overlooking the Pacific Ocean, offering incredible views and unmatched beach access. Seabrook is a thoughtfully-built new town founded on new urbanism design.

Seabrook features over 475+ Washington Coast homes in eight neighborhoods, some available as vacation rentals and some available for purchase, as well as numerous merchants, more than 30 parks, a Town Hall, and countless amenities. Seabrook is a walking and biking paradise! Designed with a “walk to anything in five minutes” principle in mind, guests and residents routinely comment on the thoughtful design their team has employed to create this unique vacation town.

Every year, thousands of guests stay at Seabrook by booking one of the over 270 homes in their popular Vacation Rentals program. No home is the same, accommodating anywhere from two to twenty people (dogs, too, in certain homes).

In addition to promenades and walking trails galore, you’ll find a central amphitheater, a hilltop and oceanfront park, outdoor games and playgrounds, a Town Hall, fire pits, horseshoe pits, mountain bike trails, a heated indoor pool, and spacious Crescent Park. Leave the car in park and explore simple living on the Washington Coast.

All of the homes come with well-appointed kitchens, but we all know that grabbing a bite to eat while on vacation is a bonus. Whether you’re looking for a romantic dinner, a family-friendly meal, or coffee before a beach walk, Seabrook offers dining options for every taste, all within an easy stroll of the town center.

- Frontager’s Pizza Co. – Wood-fired pizza, pasta, salads, local beer & wine.

- Koko’s Restaurant & Tequila Bar – Elevated Mexican cuisine, craft margaritas, weekend brunch.

- Rising Tide Tavern – Burgers, seafood, fish & chips, salads, and local brews.

- The Stowaway Wine Bar – Wine, charcuterie, and small plates in a cozy setting.

- Vista Bakeshop – Fresh pastries, breakfast sandwiches, artisan breads, and coffee.

- Bellwether Cafe – Espresso drinks, breakfast, sandwiches, and grab-and-go options.

- The Sweet Life – Ice cream, candy, fudge, and milkshakes.

SEABROOK AND THE ART OF TOWNMAKING

Town founders, Casey and Laura Roloff, first met in high school and quickly realized they had one major thing in common — they loved the beach! After graduating from college, they married and moved to the Oregon Coast, where they started their very first business painting houses.

As the Roloffs became more involved in the local community, they studied the local and national real estate markets and recognized an opportunity to build custom vacation homes, second homes, and primary residences that had architectural character and an uncommon attention to detail.

Using new urbanist design principles and inspiration from the internationally recognized town of Seaside, Florida, they set out to build their first beach community, Bella Beach, on the Oregon Coast. Finding great success with Bella, they eventually looked northward towards Washington State for a similar opportunity. This led them to Grays Harbor County, where, in 2004, along with their innovative design team, they worked collaboratively to curate and develop Washington’s most celebrated beach town, Seabrook.

A TOWN WITH A PEDESTRIAN-FRIENDLY SCALE

Visitors to Seabrook experience how the lost art of town making has been brought to life with a specialized design concept known as The New Urbanism. Everything in the coastal town is purpose-built with walkability and connectivity intertwined with the beautiful coastal surroundings, a signature of the Pacific Northwest.

Entering Seabrook is stepping into a welcoming, comfortable and charming atmosphere that has all been carefully planned and accomplished one home, retail space, amenity, or trail at a time. Yes, cars are welcome (how else are you going to get there?), but you’ll be happy to leave them stowed away in a carriage house or along one of the tree-lined streets where on-street parking is actually encouraged to ensure safe streets for pedestrians and bicyclists.

INTENTIONAL EASE OF ACCESS

The transect concept provides zones that are an important part of new urbanism planning and that help describe the wide range of community transitions from rural to urban with an emphasis of increasing town-wide accessibility to homes, shopping, and amenities.

Proximity To Metropolitan Areas

Seabrook is conveniently located a short drive away from Seattle and Portland, making it an accessible drive-to vacation location that has been on-the-rise for years. The beach town is also situated near popular sightseeing destinations like the Olympic National Park (a World Heritage Site), a 45-minute drive away.

Homes to Accommodate Everyone

Seabrook was built with inclusivity in mind. Homes of all sizes, from 2-person carriage homes to homes that sleep upwards of 20 people, create a sense of community for everyone living or staying in Seabrook.

Merchants & Town Events

In Seabrook, children play freely and safely, merchants quickly become staple stops of old and new patrons alike, and events bring the community together for conversation and memories made. They even have venues you can rent for your own special events such as a wedding.

Miles of Shoreline and Trails to Explore

But we can’t forget about the beach. All roads (or, in Seabrook’s case, walking trails) flow down to the magnificent allure of the Pacific Ocean. Seabrook’s three beach accesses provide a convenient way to enjoy and access the beach from its three oceanfront neighborhoods: NW Glen, Pacific Glen, & Elk Creek.

Community Involvement

The connectivity also expands throughout the local community and county. The Seabrook Community Foundation awards grants to many Grays Harbor County Nonprofits with an emphasis on aiding Grays Harbor Youth. One percent of every house sale goes towards the efforts to uplift the North Beach community that surrounds Seabrook.

I highly encourage you if you have a blank space in your calendar this summer or any other time of the year to visit Seabrook. Its charm, connection to nature, and easy access from the city makes it a great place to invest your vacation dollars. If you are interested in exploring the real estate market there, please reach out. I have connections to the sales team now that they are a Windermere affiliate. Here’s to a beautiful summer ahead and finding some time to wind down with the people that matter most.

Design Trends for 2026 & Beyond: Softer, Lived-In Luxury

As we find ourselves in the midst of spring, freshening up our surroundings is a natural inclination. If you have been dreaming of updating your space, trying something new, or just want an overall refresh, I’ve uncovered the latest trends to help inspire your next project. Don’t miss all the fun links below that help bring these trends to life.

As a broker who is in and out of hundreds of homes a year, I can definitely say these simple pivots can add enjoyment plus resale value to your home. Many of these design trends can be done on your own or involve minor changes that make a big impact without breaking the bank. Some are more involved, but if you are considering a remodel, these great tips will help ensure your investment is on track.

The biggest home design trends for 2026 are all about warmth, texture, personality, and nature-inspired living. After years of ultra-minimal, gray-and-white interiors, designers are moving toward homes that feel layered, emotional, and timeless rather than overly “perfect.”

Here’s a breakdown of the top trends across paint, decor, surfaces, kitchens, baths, and landscaping.

- Paint Color Trends for 2026

Warm Earthy Neutrals Replace Cool Gray

Designers are calling these “grounding neutrals. The dominant palette for 2026 is:

- warm taupe

- mushroom

- khaki

- camel

- espresso brown

- clay and terracotta

- olive and eucalyptus greens

Most talked-about tones:

- Sherwin-Williams “Universal Khaki”

- Benjamin Moore “Silhouette” (deep espresso-charcoal)

- Valspar “Warm Eucalyptus”

- rich browns and muddy greens

Best Seattle-Friendly Paint Colors

These work especially well in cloudy PNW lighting:

- Benjamin Moore Swiss Coffee

- Benjamin Moore White Dove

- Benjamin Moore Pale Oak

- Benjamin Moore Edgecomb Gray

- Sherwin-Williams Alabaster

- Sherwin-Williams Accessible Beige

- Sherwin-Williams Drift of Mist

- Sherwin-Williams Greek Villa

- Sherwin-Williams Shoji White

Color Drenching Continues

Color drenching, which involves rooms painted in a single tone, including walls, ceilings, trim, and cabinetry, is still trending strongly in 2026. This creates a cocoon-like, luxurious feel. Popular drenched colors:

Soft Pastels Are Back, But Sophisticated

Soft pastels are being used in a more grown-up, vintage-inspired way rather than in a playful or childish way. Popular colors that add warmth and softness are:

- Interior Decor Trends

“Lived-In Luxury”

Lived-in Luxury is a design style that makes a home feel elevated, beautiful, and curated, but also comfortable, warm, personal, and actually livable. The aesthetic is cozy sophistication instead of sterile minimalism. Homes are becoming:

- softer

- more personal

- less staged

- more collected over time

Expect:

- antiques mixed with modern

- handmade pottery

- layered textiles

- books everywhere

- artisan lighting

- vintage rugs

Curves & Organic Shapes

Sharp modern edges are softening. The aesthetic in 2026 includes:

Statement Lighting as Art

Lighting is now treated like jewelry for the room rather than a utility. I’ve been impressed with lighting options that are not overly expensive, and the impact that is made is huge. Simply replacing a “boob” light in a bedroom with something more elevated or a bar light above a bathroom mirror that has more appeal can change the feel of the entire room and elevate it. Lighting is becoming sculptural:

Chrome Is Back

Warm brass still exists, but polished chrome and nickel are returning in a cleaner, more timeless way. I am also seeing a trend of mixed metals rise to the top. Along with the layered, more collected look, having a balanced variety instead of just one tone throughout creates a cozier, more interesting space.

Especially trending in:

- kitchens

- baths

- cabinet hardware

- faucets

Wallpaper is no longer just “pattern.”

Wallpaper is having a MASSIVE moment in 2026, but it looks very different from the wallpaper trends people remember from the 1990s or even the accent-wall era of the 2010s. The biggest shift is that it’s becoming immersive, tactile, and soulful. Expect:

- texture

- atmosphere

- architecture

- storytelling

- emotional design

- Hard Surface Trends

Natural Stone with Movement

While new paint, switching out hardware, and updating lighting can be somewhat easy and less costly, new hard surfaces are a bigger investment. If you are considering replacing your countertops, choosing dramatic natural stone instead of plain quartz is the direction we are seeing designers go. The more movement and organic texture, the better. Even a quartz with some veins has been popular versus something more plain.

Trending:

Warm Woods Dominate

White oak remains huge, but darker woods are rising:

- walnut

- smoked oak

- medium brown woods

- rich paneling

Warm wood paneling is especially trending in mid-century modern homes and recently-built modern new construction homes. Gone are the days when wood paneling is frowned upon. I’m even seeing older homes that still have original wood paneling be preserved and highlighted. There are really fun wood paneling kits that are available to do an accent wall, stairwell, or end of a hallway to add depth, texture, and warmth.

Textured Finishes

Flat, sterile finishes are fading, and imperfection is now considered luxurious. This aligns with the more curated, collected feel that lends itself to coziness and evokes emotion.

Trending textures:

- limewash walls

- Venetian plaster

- fluted wood

- Zellige tile

- handmade ceramic tile

- textured stone

Tile Trends

Personalized tilework is becoming a major design feature. Tiles with texture, warmth, and variation can make a room feel softer and less stark. Zellige tile, which is intentionally irregular (has differing tile height and imperfect edges), glossy, and reflects light, can be found in whites and creams or in tonal shades, which are big in 2026:

- checkerboard stone

- mosaic tile

- slab backsplashes

- handmade-look tile

- full-height stone walls

- Kitchen Trends

“Soft Kitchens”

Kitchens are becoming warmer and less clinical. Completely white modern kitchens are being replaced with warmer, layered kitchens. Creams and wood are highlights to create dimension, character, and warmth.

Trending:

- wood cabinetry

- creamy paint colors

- hidden appliances

- furniture-style islands

- mixed materials

Mixed Cabinet Colors

Instead of one uniform kitchen look, updates are added to create a very custom-looking space with mixed cabinet colors. As I mentioned above, a mix of hardware and paint can help bring a space to life and add character and charm. This should be done in a well-balanced way to provide a consistent, curated feel.

Integrated Wellness Features

The home is becoming more wellness-centered. Creating spaces to slow down, simplify, and center in health are increasingly popular. Favorite wellness features for kitchens include:

- beverage stations

- hidden pantries

- indoor herb gardens

- filtered water systems

- calming breakfast nooks

- Bathroom Trends

Spa-Like Natural Bathrooms

Bathrooms are becoming retreat spaces and feel more spa-like versus utilitarian. Huge movement toward softening the space by using:

- warm stone

- soft lighting

- plaster finishes

- natural wood vanities

- wet rooms

- freestanding tubs

Statement Stone Slabs

Large slab walls and dramatic stone vanities are replacing busy tile patterns.

Especially popular:

- travertine

- marble-look quartzite

- green-veined stone

- Exterior & Landscaping Trends

Nature-Inspired Exteriors

Exterior palettes are becoming softer, earthier, and more architectural. This is probably the question I am most often asked, “what color should I paint my house?”. Darker exterior colors have been on the rise for some time, and they continue to stay there, but with a bend towards earth tones such as sage green, olive green, warm white, mushroom brown, and charcoal brown.

Trending colors:

- Sherwin-Williams Evergreen Fog

- Sherwin-Williams Pewter Green

- Benjamin Moore White Dove

- Benjamin Moore Pale Oak

- Sherwin-Williams Urbane Bronze

Landscaping Becomes More Organic

The “perfect manicured yard” is fading and leaning towards more organic landscapes. People want landscaping that feels connected to nature and has lower maintenance.

Trending:

- native plants

- meadow-style gardens

- layered greenery

- drought-tolerant landscaping

- edible gardens

- natural stone paths

Outdoor Living Rooms

Backyards are increasingly designed like interior spaces. Indoor-outdoor living was a big trend that was identified during Covid and stuck. It is still growing strongly, and a feature that creates expanded enjoyment and a great ROI when selling.

- outdoor kitchens

- lounge furniture

- fire pits

- pergolas

- textured lighting

- integrated dining spaces

The Overall 2026 Aesthetic

The big shift is from cold minimalism, gray everything, and ultra-modern perfection to warmth and layered texture that evoke emotional comfort by using nature-inspired materials, individuality, and timelessness. Designers are calling it organic modern, lived-in luxury, earthy vibrancy, and modern heritage. I hope this overview of the latest 2026 design trends has created some inspiration, whether you’re looking to make some minor, impactful tweaks or to embark on a remodel. Please reach out if you need access to some trusted vendors who can help you bring your vision to life.

Market Realities & Opportunities: Equity Growth, Improved Affordability & Overall Stability

With so many headlines about the housing market right now, I wanted to give you a clear, local, data-backed update, specifically breaking down what’s happening in King and Snohomish counties. While the national conversation can feel uncertain, the local numbers tell a much more grounded story.

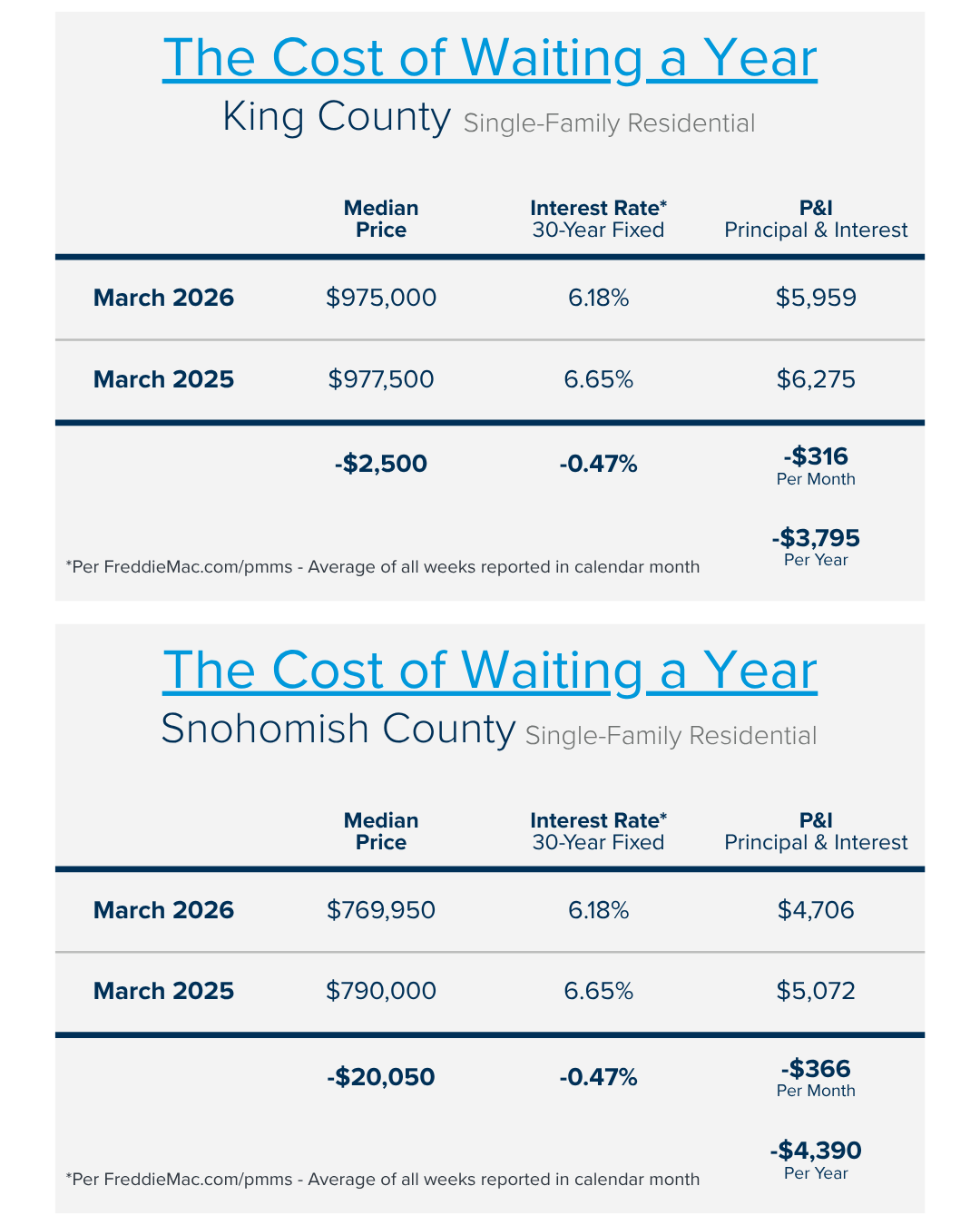

The biggest disruption we have experienced so far this year was the increase in interest rates since the US conflict with Iran began on February 28th. Let’s put this in perspective. Pre-conflict, rates hit 5.99%, the lowest they have been since the summer of 2022, and they quickly jumped to 6.59% by March 23, 2026, and on April 27th, 2026 settled around 6.3%. All in all, they took a quick jump up, but have seemed to settle over the last few weeks.

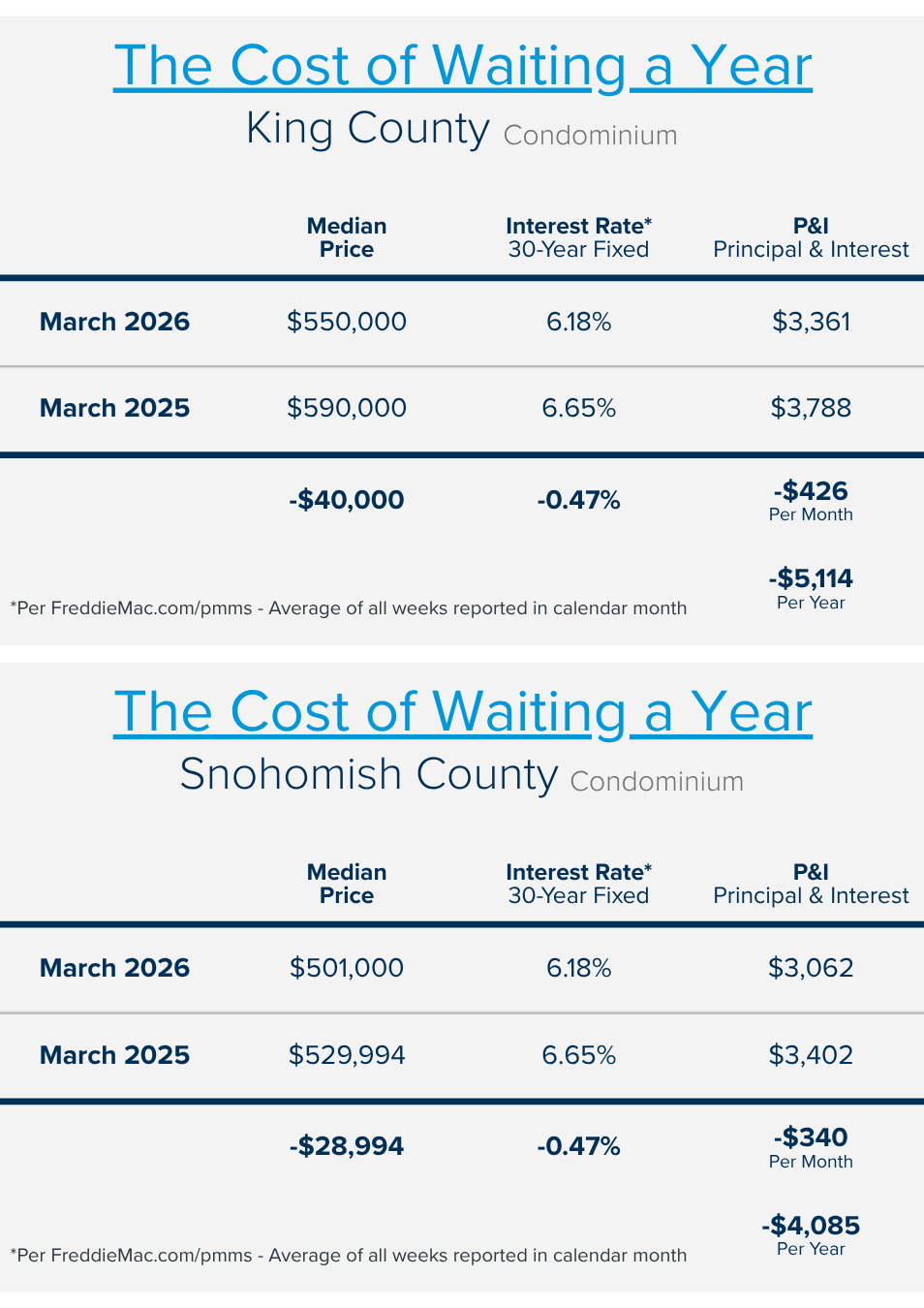

While it was awesome to see 5.99% and the recent increase was disappointing, it’s important to also look back and understand that it is still more affordable to buy now compared to last year and the year prior. A year ago, on April 28th, 2025, rates were 6.83%, and on April 29th, 2024, they were 7.4%! This is a dramatic difference in favor of buyers now, coupled with flat prices year-over-year. Check out the charts below for both King and Snohomish Counties for Single-Family Residential Homes, which show the real numbers surrounding monthly payments.

With payments $316 lower in King County year-over-year and $366 lower in Snohomish County, this is a welcome relief for buyers. Further, check out the charts below for the year-over-year savings for Condominiums: $426 and $340, respectively. This is especially beneficial for first-time homebuyers who will often purchase this property type based on affordability.

The Big Picture: Still a Seller’s Market in Both Counties

Despite more inventory coming on the market, both counties are still in seller’s market territory for Single-Family Residential Homes:

- King County: ~1.8 months of inventory (0-2 months = Seller’s Market, 2-4 = Balanced Market, 4+ = Buyer’s Market)

- Snohomish County: ~1.7 months of inventory

- Translation: Even with more listings, there are still not enough homes to meet demand.

- Sellers should note that the homes that are being sold are properly prepared for market with accurate pricing.

Inventory: Rising, But Not Oversupplied

You may be hearing that inventory is “up”, and that’s true. Here’s what that actually looks like locally for Single Family Residential Homes:

King County:

- Available homes for sale in March 2026 are up 41% year-over-year .

- New listings in March 2026 are up 13% year-over-year.

- Month-to-date in April 2026, available homes for sale are up 19% over March 2026.

Snohomish County:

- Available homes for sale in March 2026 are up even more, 46% year-over-year.

- New listings in March 2026 are up 11% year-over-year.

- Month to date in April 2026, available homes for sale are also up 19% over March 2026

What this means:

- Buyers have more choices than last year, and inventory is building.

- But we’re still below a balanced market, which is why prices are holding.

Home Prices: Stable!

This is where headlines often get it wrong.

King County Single Family Residential:

- Median price in March 2026: ~$1,000,000 (up 1% year-over-year)

- Prices are largely stable with slight upward pressure.

Snohomish County Single Family Residential:

- Median price in March 2026: ~$775,000 (up 1% year-over-year)

- More affordability, but still seeing modest appreciation.

Key takeaway:

This isn’t a declining market; it’s a normalizing one after rapid growth, with both counties still showing price stability.

Home Equity is High, and Real Estate is a Proven Investment:

The price growth for Single-Family Residential Homes since 2020 in King County has been 35%, and in Snohomish County, 47%. Even more so, prices have increased 84% over the last 10 years in King County and by 100% in Snohomish County.

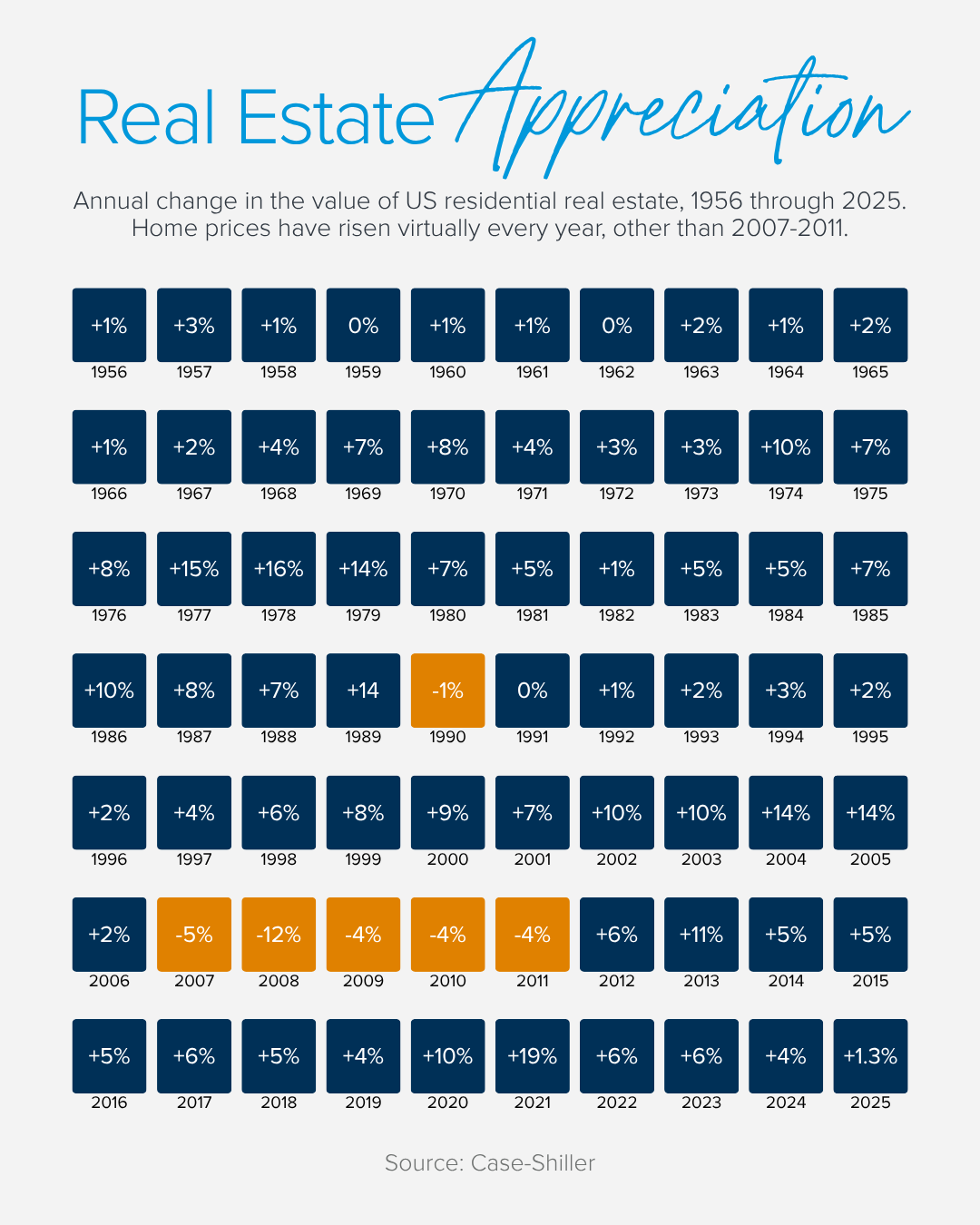

Further, check out this chart below, which shows the national figures on equity growth since 1956. Real estate has proven to be one of the best long-term investments a person can make, which leads to building strong household and generational wealth.

Market Speed: Homes Are Still Moving

Even with more inventory, homes are still selling at a steady pace:

- King County: ~33 days on market in March and ~ 28 days in April month-to-date.

- Snohomish County: ~37 days on market in March and ~ 29 days in April month-to-date.

And homes are still selling very close to asking:

- King County: ~99% of original list price.

- Snohomish County: ~98% of original list price.

Well-priced homes that are expertly prepared for market are the ones that are moving quickly and seeing less negotiations, especially in desirable neighborhoods.

What This Means for You

If you’re a buyer:

- You have more options than last year.

- But competition hasn’t disappeared.

- Waiting for rates to drop could mean more buyers entering at once, which will drive competition and create higher prices.

If you’re a seller:

- You’re still in a strong position, equity growth has been abundant over the last 5-10 years, consistent over the last 7 decades.

- Pricing correctly matters more than it did in the peak frenzy.

- Homes are selling, but buyers are more selective.

Bottom Line

The headlines may sound dramatic, but the local reality is much more balanced:

- Inventory is improving, but is still limited.

- Prices are holding steady.

- Demand remains strong across both counties.

If you’re thinking about making a move, or just want to understand how this applies to your specific situation, I’m always happy to help you interpret the numbers. Please reach out if you’d like to learn more. I can apply these figures to your property type, location, and price point to help you understand the market more clearly. Clarity is key to empowering strong decisions, and I always lead with the data to provide sound guidance.

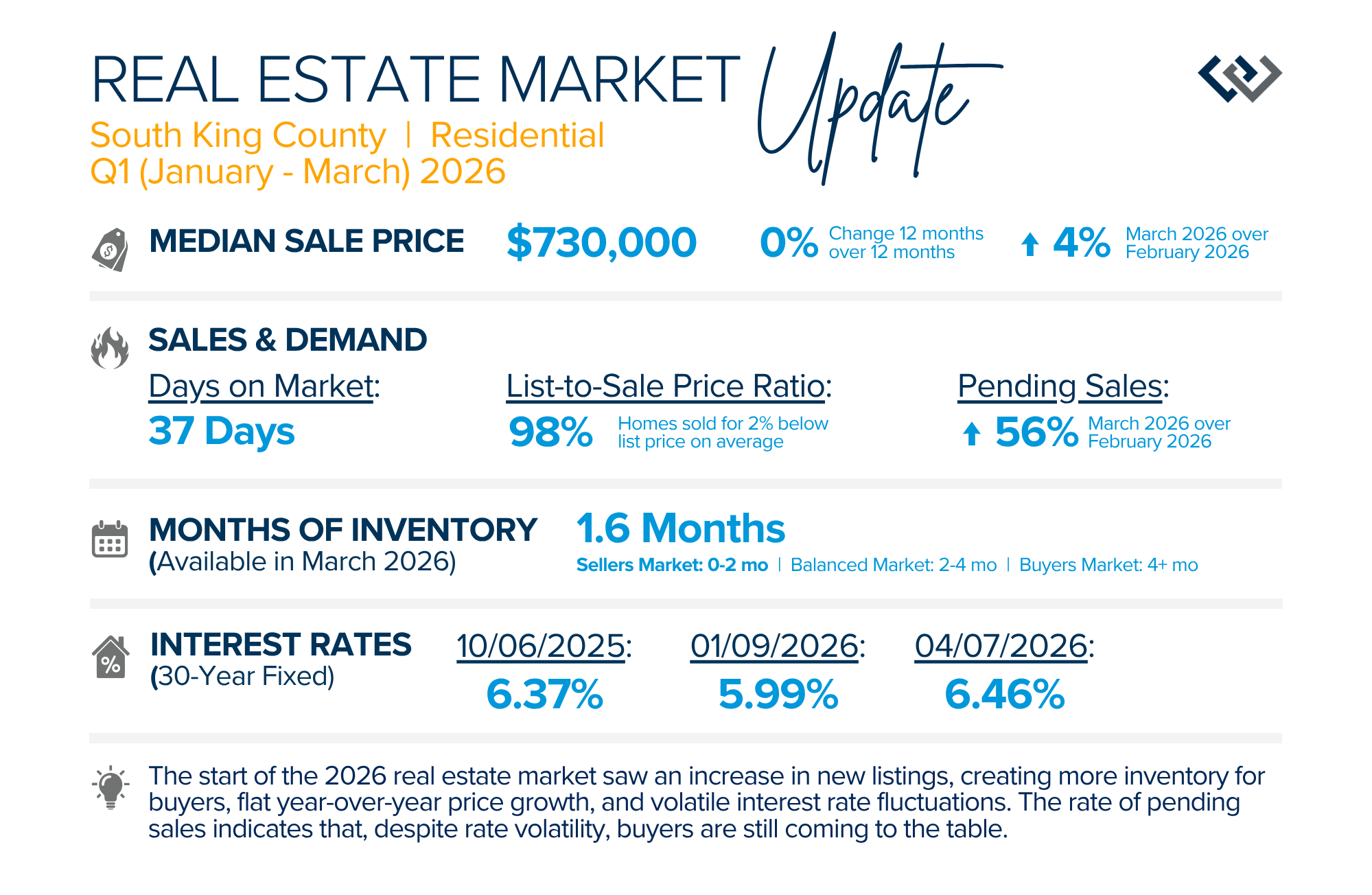

QUARTERLY REPORTS Q1 2026

The start of the 2026 real estate market saw an increase in new listings, creating more inventory for buyers, flat year-over-year price growth, and volatile interest rate fluctuations. As we finished Q1, prices began their seasonal uptick month-over-month, with pending sales also starting to rise. With more selection, the market is favoring well-prepared homes that are priced accurately.

Flat year-over-year price growth has helped affordability, but the latest rise in interest rates could moderate the month-over-month growth as we head into Q2. The rate of pending sales indicates that, despite rate volatility, buyers are still coming to the table. Seller equity remains high, with over half of all homeowners having at least 50% equity.

If you are curious about how today’s trends align with your real estate goals, please reach out. It is always my goal to help keep my clients informed to empower strong decisions.

Why Home Preparation and Staging Matter More Than Ever

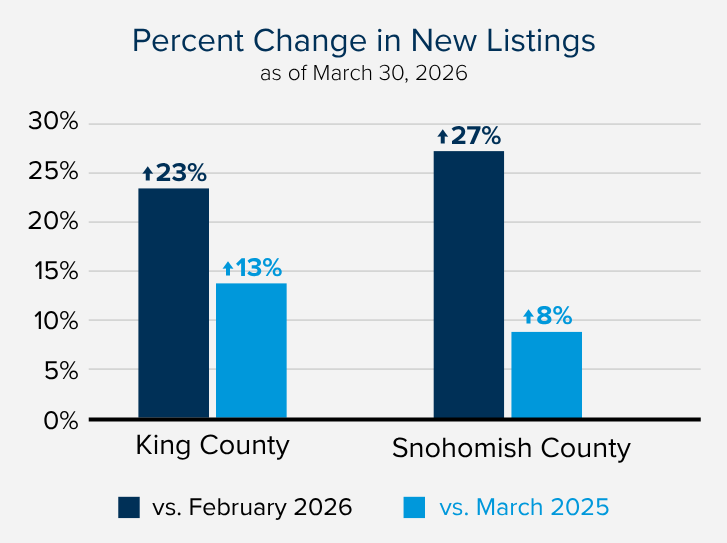

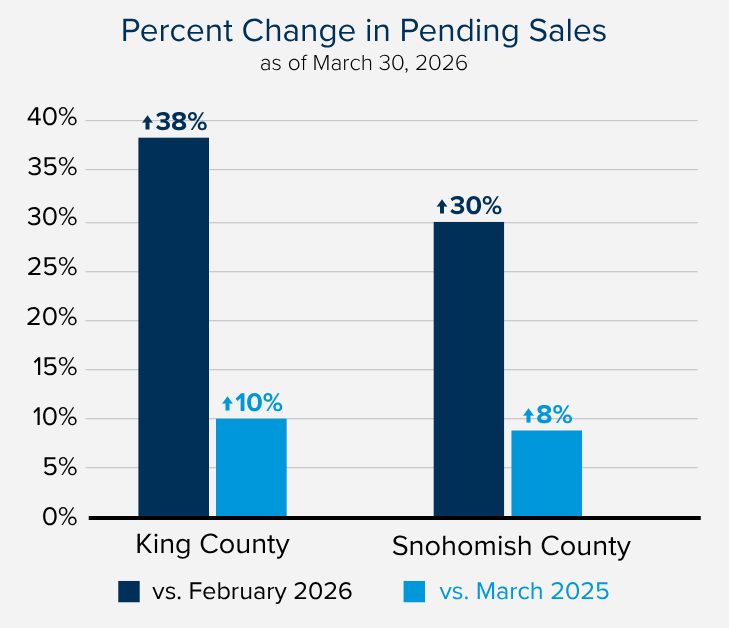

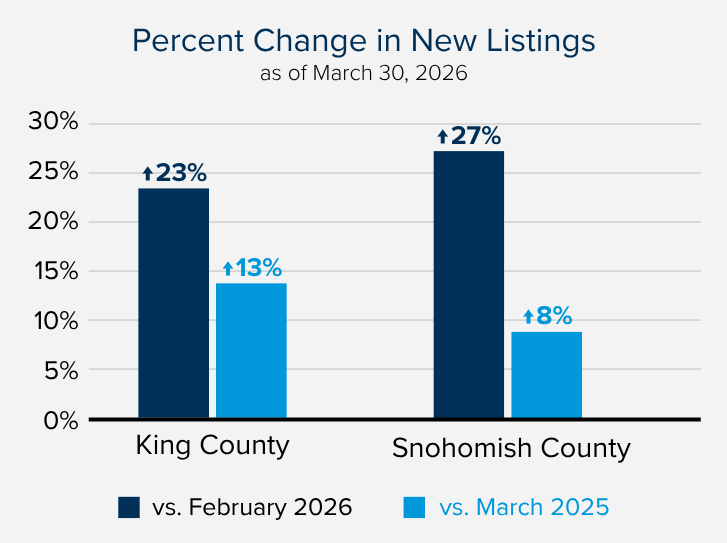

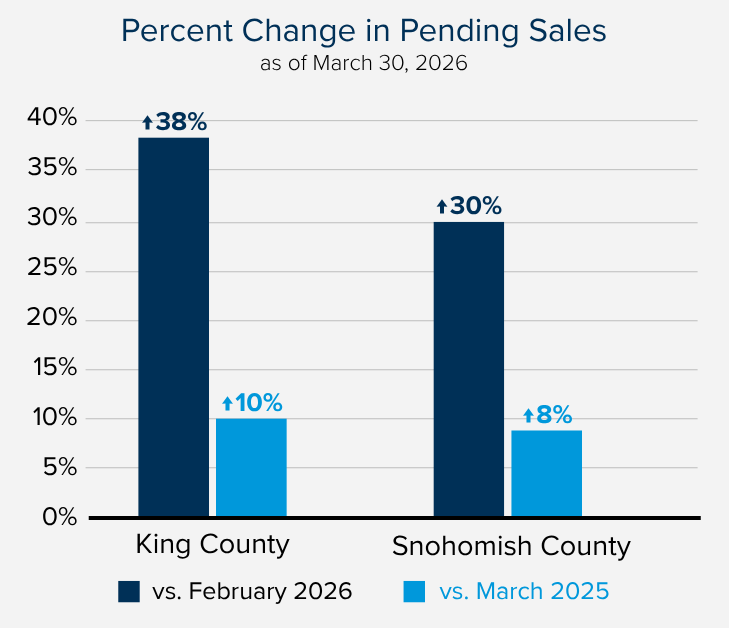

In today’s market, buyers have more options, and with affordability challenges, they’re more selective than ever. That means first impressions aren’t just important… they’re everything. In fact, as of March 30th, 2026, month-to-date new listings are up in King County by 23% over February 2026, and up 13% over March 2025. In Snohomish County they are up 27% over February 2026 and up 8% over March 2025. This means your listing needs to stand out to win!

One important thing to note is how the rate of pending sales is tracking with the new listings as we finish out Q1 and head into the busy Q2 months. Pending sales were up 38% in King County and up 30% in Snohomish County month-to-date in March 2026 over February 2026. They were also 10% higher in King County and 8% higher in Snohomish County over March of last year. While this increase is positive, it is critical that home sellers understand the impact that thorough home preparation, strategic staging, and accurate pricing have on buyer decisions. While pending sales are up, there are many listings lingering on the market and not selling, so curated market preparation is key.

Buyers are very much focused on what the monthly payment will be as they reconcile the current interest rate with their down payment. In 2025, according to the National Association of Realtors, down payments were at an all-time high, leaving less money for buyers after closing to make improvements or repairs. This has put pressure on sellers to bring an appealing move-in-ready home to market. This eliminates roadblocks for buyers, so they feel financially secure in their purchase as they take on the new monthly payment and deplete their savings.

This is why the work that is done before the sign goes in the yard is the most impactful and leads to the highest return for sellers. This starts with a detailed walk-through of the property, looking at it through the buyers’ eyes. This will lead the market preparation, along with performing a pre-listing inspection, which will help unearth any issues that we can address before listing. That preparation could result in executing the repairs, pricing accordingly, or having a plan for buyer negotiations ahead of time, eliminating surprises and lack of seller control.

This is an important step in getting the listing ready for market and creating optimal results versus having a buyer discover issues during a pending sale with an inspection contingency when buyer remorse is at its highest! It shifts the power dynamic to the seller through transparency to harness the controllable aspects of negotiations ahead of time. It also ensures they do not lose their buyer haggling over repairs during an inspection negotiation when a buyer cannot or will not take on further expenses after closing due to affordability. The upfront transparency builds trust amongst the parties and enables the buyer to connect with the property with clarity. Instead of the buyer falling in love with the house, making an offer, and then picking it apart during an inspection contingency, and the home losing its luster and/or inviting adversarial negotiations.

Bringing a well-prepared, well-priced, neutral home to market will lead to more buyer traffic, which will often generate stronger offers and possible price escalation through buyer competition. This strategy highlights the home’s value and makes it stand out amongst the crowd. With more listings coming to market each week as we head into the brisk spring market, these steps ensure you make the best first impression and get the highest return.

Recent data from the National Association of Realtors highlights a clear trend: how a home looks and feels directly impacts how it sells.

Buyers Need Help Seeing the Potential

Most buyers aren’t able to visualize a home’s full potential on their own.

- 83% of buyers’ agents say staging makes it easier for buyers to see a property as their future home.

When a home is thoughtfully prepared, it removes uncertainty, and that confidence often translates into stronger offers.

Staging Can Influence Your Bottom Line

In the Greater Seattle market, where pricing strategy is critical and buyers are more selective, presentation plays a direct role in outcomes.

- While national data shows staged homes may receive 1–5% higher offers, results in higher-priced markets like ours are often more significant. Many local agents see staging translate into tens of thousands of dollars in added value, along with stronger, cleaner terms. Price matters, and good terms get transactions to close!

- Staged homes also tend to generate faster early activity, shorter days on market, and fewer price reductions, helping sellers maintain leverage in a more competitive environment.

With affordability top of mind for buyers, creating an emotional connection isn’t just impactful, it can be the difference between a hesitant buyer and a motivated one willing to act decisively.

The Rooms That Matter Most

Not all spaces carry equal weight. Buyers focus heavily on:

- Living Room

- Primary Bedroom

- Kitchen

These are the areas where staging has the greatest impact, and where we focus our efforts to tell the strongest story. Also, if a floor plan could lend to multiple options, we will choose to highlight the use of the rooms towards the latest buyer trends. Such as an at-home office, extended outdoor living space, or guest room, or multi-generational living. If a room has spatial challenges, staging can help solve the use of space for the buyer.

It’s Not Just Staging – It’s Marketing

Today’s buyers start their search online, and expectations are high.

- 73% of buyers say digital marketing is critical.

- Video, virtual tours, floorplans, and staging all enhance the on-line experience and inspire buyers to go see the property in-person.

In fact, nearly half of buyers expect homes to look like what they see on TV, and many are disappointed when they don’t. That means your home isn’t just competing with other listings, it’s competing with expectations.

The Investment Is Strategic

The typical staging investment is relatively modest compared to the potential return. It is important that staging is viewed as an investment, not an expense, as an investment provides a return and expenses do not:

- According to RESA (Real Estate Staging Association), the average investment in staging is $3,500–$4,400, while in the higher-priced Seattle market, that investment often ranges from $3,000 to $7,500+, depending on the size and value of the home.

- With home values where they are, staging is often less than 1% of the list price, but can have a meaningful impact on buyer demand, speed of sale, and final price. I’ve seen this with my listings and through the eyes of buyers I work with.

- Staging can vary from whole vacant homes, edit staging, or partial staging; each strategy is built around the specific scenario.

In a more competitive market, this isn’t just an upgrade, it’s a strategy.

The Bottom Line

With more homes on the market and buyers feeling the pressure of affordability, presentation is no longer optional, it’s essential.

Staging helps your home:

- Stand out online.

- Connect emotionally with buyers.

- Compete effectively.

- Maximize your final sale price.

Thinking About Selling?

I’d be happy to walk you through what preparation and positioning could look like for your home, and help you build a strategy to have your home stand out in today’s market. I have a robust list of trusted contractors, vendors, inspectors, and stagers who help execute this process.

I also have access to quick home equity loan programs through Windermere Ready that help sellers access funds to make repairs and prepare their home to shine. Lastly, I am very involved with helping oversee the process and making it as seamless and profitable as possible. It is always my goal to listen and learn about my clients’ goals and help them chart the best path to success.

Why Home Preparation and Staging Matter More Than Ever

In today’s market, buyers have more options, and with affordability challenges, they’re more selective than ever. That means first impressions aren’t just important… they’re everything. In fact, as of March 30th, 2026, month-to-date new listings are up in King County by 23% over February 2026, and up 13% over March 2025. In Snohomish County they are up 27% over February 2026 and up 8% over March 2025. This means your listing needs to stand out to win!

One important thing to note is how the rate of pending sales is tracking with the new listings as we finish out Q1 and head into the busy Q2 months. Pending sales were up 38% in King County and up 30% in Snohomish County month-to-date in March 2026 over February 2026. They were also 10% higher in King County and 8% higher in Snohomish County over March of last year. While this increase is positive, it is critical that home sellers understand the impact that thorough home preparation, strategic staging, and accurate pricing have on buyer decisions. While pending sales are up, there are many listings lingering on the market and not selling, so curated market preparation is key.

Buyers are very much focused on what the monthly payment will be as they reconcile the current interest rate with their down payment. In 2025, according to the National Association of Realtors, down payments were at an all-time high, leaving less money for buyers after closing to make improvements or repairs. This has put pressure on sellers to bring an appealing move-in-ready home to market. This eliminates roadblocks for buyers, so they feel financially secure in their purchase as they take on the new monthly payment and deplete their savings.

This is why the work that is done before the sign goes in the yard is the most impactful and leads to the highest return for sellers. This starts with a detailed walk-through of the property, looking at it through the buyers’ eyes. This will lead the market preparation, along with performing a pre-listing inspection, which will help unearth any issues that we can address before listing. That preparation could result in executing the repairs, pricing accordingly, or having a plan for buyer negotiations ahead of time, eliminating surprises and lack of seller control.

This is an important step in getting the listing ready for market and creating optimal results versus having a buyer discover issues during a pending sale with an inspection contingency when buyer remorse is at its highest! It shifts the power dynamic to the seller through transparency to harness the controllable aspects of negotiations ahead of time. It also ensures they do not lose their buyer haggling over repairs during an inspection negotiation when a buyer cannot or will not take on further expenses after closing due to affordability. The upfront transparency builds trust amongst the parties and enables the buyer to connect with the property with clarity. Instead of the buyer falling in love with the house, making an offer, and then picking it apart during an inspection contingency, and the home losing its luster and/or inviting adversarial negotiations.

Bringing a well-prepared, well-priced, neutral home to market will lead to more buyer traffic, which will often generate stronger offers and possible price escalation through buyer competition. This strategy highlights the home’s value and makes it stand out amongst the crowd. With more listings coming to market each week as we head into the brisk spring market, these steps ensure you make the best first impression and get the highest return.

Recent data from the National Association of Realtors highlights a clear trend: how a home looks and feels directly impacts how it sells.

Buyers Need Help Seeing the Potential

Most buyers aren’t able to visualize a home’s full potential on their own.

- 83% of buyers’ agents say staging makes it easier for buyers to see a property as their future home.

When a home is thoughtfully prepared, it removes uncertainty, and that confidence often translates into stronger offers.

Staging Can Influence Your Bottom Line

In the Greater Seattle market, where pricing strategy is critical and buyers are more selective, presentation plays a direct role in outcomes.

- While national data shows staged homes may receive 1–5% higher offers, results in higher-priced markets like ours are often more significant. Many local agents see staging translate into tens of thousands of dollars in added value, along with stronger, cleaner terms. Price matters, and good terms get transactions to close!

- Staged homes also tend to generate faster early activity, shorter days on market, and fewer price reductions, helping sellers maintain leverage in a more competitive environment.

With affordability top of mind for buyers, creating an emotional connection isn’t just impactful, it can be the difference between a hesitant buyer and a motivated one willing to act decisively.

The Rooms That Matter Most

Not all spaces carry equal weight. Buyers focus heavily on:

- Living Room

- Primary Bedroom

- Kitchen

These are the areas where staging has the greatest impact, and where we focus our efforts to tell the strongest story. Also, if a floor plan could lend to multiple options, we will choose to highlight the use of the rooms towards the latest buyer trends. Such as an at-home office, extended outdoor living space, or guest room, or multi-generational living. If a room has spatial challenges, staging can help solve the use of space for the buyer.

It’s Not Just Staging – It’s Marketing

Today’s buyers start their search online, and expectations are high.

- 73% of buyers say digital marketing is critical.

- Video, virtual tours, floorplans, and staging all enhance the on-line experience and inspire buyers to go see the property in-person.

In fact, nearly half of buyers expect homes to look like what they see on TV, and many are disappointed when they don’t. That means your home isn’t just competing with other listings, it’s competing with expectations.

The Investment Is Strategic

The typical staging investment is relatively modest compared to the potential return. It is important that staging is viewed as an investment, not an expense, as an investment provides a return and expenses do not:

- According to RESA (Real Estate Staging Association), the average investment in staging is $3,500–$4,400, while in the higher-priced Seattle market, that investment often ranges from $3,000 to $7,500+, depending on the size and value of the home.

- With home values where they are, staging is often less than 1% of the list price, but can have a meaningful impact on buyer demand, speed of sale, and final price. We’ve seen this with our listings and through the eyes of buyers we work with.

- Staging can vary from whole vacant homes, edit staging, or partial staging; each strategy is built around the specific scenario.

In a more competitive market, this isn’t just an upgrade, it’s a strategy.

The Bottom Line

With more homes on the market and buyers feeling the pressure of affordability, presentation is no longer optional, it’s essential.

Staging helps your home:

- Stand out online.

- Connect emotionally with buyers.

- Compete effectively.

- Maximize your final sale price.

Thinking About Selling?

We’d be happy to walk you through what preparation and positioning could look like for your home, and help you build a strategy to have your home stand out in today’s market. We have a robust list of trusted contractors, vendors, inspectors, and stagers who help execute this process.

We also have access to quick home equity loan programs through Windermere Ready that help sellers access funds to make repairs and prepare their home to shine. Lastly, we are very involved with helping oversee the process and making it as seamless and profitable as possible. It is always our goal to listen and learn about our clients’ goals and help them chart the best path to success.

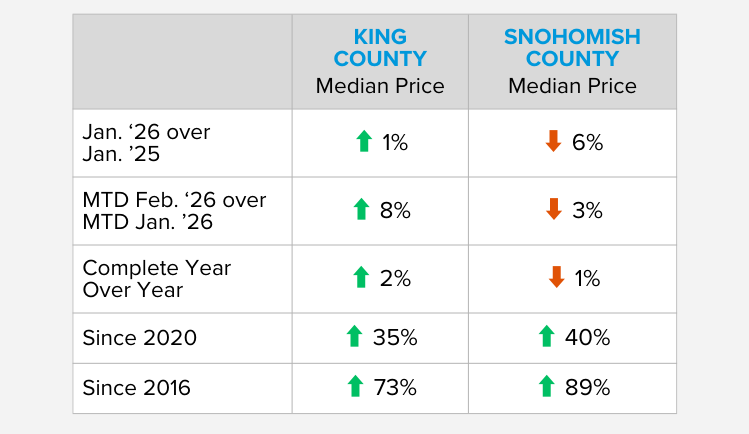

February Stats for King & Snohomish Counties Have Posted and There is a Story to Tell!

We are starting to see the normal, seasonal uptick in new listings as winter starts to thaw and the trees start to bud. The good news about this uptick in new inventory is it is up year-over-year, illustrating that more sellers are coming to market. Inventory has been pressured since the rise in interest rates, which started in 2022 and hit their peak in October 2023 at 7.91%. Since then, rates have slowly receded and are now hovering around 6%, which has helped with inventory growth and affordability.

Pending sales in February were also up, showing that buyer demand is absorbing the increase in selection. I’m also happy to report that pending sales month-to-date this March are up compared to February, by 42% in King County and 23% in Snohomish County. This mounting activity is a positive sign for the local real estate market.

Prices are steady year-over year, down 1% in Snohomish County 12-months over 12-months and up 2% in King County, and are showing signs of seasonal growth month-over-month as we head into spring. Months of inventory is up with the uptick in new listings year-over-year, but teetering from a balanced to a seller’s market, depending on the location, price point, and product. Overall, the market is healthy, fluid, and favoring well-prepared listings that are expertly priced. Buyers are ready to strike for the homes that stand out and are showing their value.

If you are curious about today’s trends and how they relate to your goals, or just love keeping up with the market, I hope you find these facts and figures helpful. If you would like to discuss them further, please reach out. It is always my goal to help keep my client well-informed to empower strong decisions.

What You Need to Know NOW: Real Time Trends for 2026 So Far

A New Year always brings new energy to the real estate market, and 2026 is already starting to show signs of growth, more movement, and a return to normalcy. After three years of slower sales due to higher interest rates, homeowners not wanting to give up their historically low interest rates, and prices remaining stable, 2026 is starting to produce some positive results in the Greater Seattle area real estate market. Some key factors that I have been tracking since the calendar flipped to 2026 that show predictive trends are the rate of:

- New Listings

- Pending Sales (Real-Time Accepted Contracts)

- Cumulative Days on Market (CDOM)

- Sales Prices to Original List Price Ratios

- Months of Inventory (Is it a Seller’s, Balanced or Buyer’s Market?)

- Interest Rates

- Price Trajectory

One of the challenges we have faced over the last three years is a lack of inventory, with many would-be home sellers staying in their homes longer in order to hold onto their low rate and payment. This has led people to stay in homes that are not the best fit for their lifestyle, and this pent-up seller demand has started to break loose. As you can see from the chart above, New Listings are up in both King and Snohomish Counties year-over-year, especially this February. This shows that for some sellers, the time has come to focus on the right fit versus payment.

Additionally, another encouraging sign is an uptick in Pending Sales (Real-Time Accepted Contracts) year-over-year and most recently during the first two weeks of February compared to the same time last year. This illustrates that buyer demand is meeting the increase in new listings and that there is a ready and willing audience wanting more selection to choose from. When the increase in pending sales starts to pace and even outpace the rate of new listings, we know there is solid demand.

The most current data above for both King and Snohomish counties shows the Cumulative Days on Market (CDOM) for the current pending sales that were accepted since January 1, 2026; more than half quickly came off the market in two weeks or less! This is a stark difference from the CDOM for closed sales in January 2026, which most likely went pending (contract accepted) in late Q4 2025. The market is waking up to the New Year with vigor and excitement for well-prepared, appropriately priced homes.

The sales price to original list price ratios are also starting to improve, inching up to 98% in the first two weeks in February 2026 from 96% in January 2026. Home sellers that are aligning with a trusted advisor to help them prepare their home for market and stay close to the data for pricing are starting to see quicker, full-price sales, and in some cases, multiple offers with price escalations. It is important to note that property condition, cleanliness, expert staging and marketing, and realistic pricing all play a critical role in garnering optimal results.

This finds us currently (MTD February 2026) in a Seller’s Market based on pending sales (0-2 Months of Inventory) in both King and Snohomish counties after only being 45 days into 2026. We calculate Months of Inventory by dividing the number of pending sales by the number of available homes for sale to determine how quickly we’d run out of inventory if no new homes came to market based on pending sales demand. We have not been at this level since April 2025 and spent the remainder of 2025 in a balanced market, so this is a marked improvement.

Interest rates are almost an entire point lower than they were last year at this time, which affords a buyer 10% more in buying power or simply results in a lower payment at the same sales price. You can view the video from Jeff Tucker, Windermere’s Chief Economist, below on what has caused interest rates to decrease. Rates declining closer to 6% and teetering towards the high 5% will unleash more demand in the market as it makes homes more affordable, and with prices maintaining, the rate matters! I think this has also led more potential home sellers to come to market as the current rates are more palatable than when they were 1-2 points higher over the last three years.

This brings us to price trajectory. With eight months of 2025 being a balanced market, rates hovering in the 7% throughout last year, and many of the homes that closed in January 2026 going under contract in late 2025, January prices recorded at lower price levels. When you take the median price over the last 12 months and compare it to the previous 12 months (complete year-over-year), prices are flat and stable.

With early indicators such as pending sales, lower rates, and faster CDOM, I anticipate more historical price growth levels in 2026, between 3-5%. I certainly do not anticipate prices lowering. In fact, we have seen list prices soften, and more home sellers who are truly motivated come to market with realistic expectations and better market preparation. The new normal is taking shape.

This uptick in market activity and return to normalcy comes on the shoulders of extreme home equity growth since 2020 and over the last 10 years. The growth is staggering! The abundance of wealth that people have in their homes is beneficial to positioning a move that better fits their lifestyle, funding a remodel, helps plan for retirement, or even an out-of-state move as long at the payment works. The recent decrease in rate and long-term equity gains have supported these exciting moves.

If you or someone you know are curious about how the latest trends, long-term growth in the market, and current rates affect your ability to make a move, please reach out. I am committed to staying close to the real-time data, assisting with discerning the information, and applying it to my clients’ goals to help them navigate big life changes. It is my mission to help keep my clients informed, so they are empowered to make strong decisions. 2026 is already starting to provide some great opportunities, and if you’d like to learn more, let’s talk!